Buy Crypto

Buy Crypto- Markets

Futures

Futures- Spot

- Copy Trade

- Earn

- More

Digital banks have long ceased to make money from traditional banking services; the real goldmine lies in stablecoins and identity authentication.

Original Article Title: Neobanks Are No Longer About Banking

Original Article Author: Vaidik Mandloi, Token Dispatch

Original Article Translation: Chopper, Foresight News

Where Is the True Value Flowing for Digital Banks?

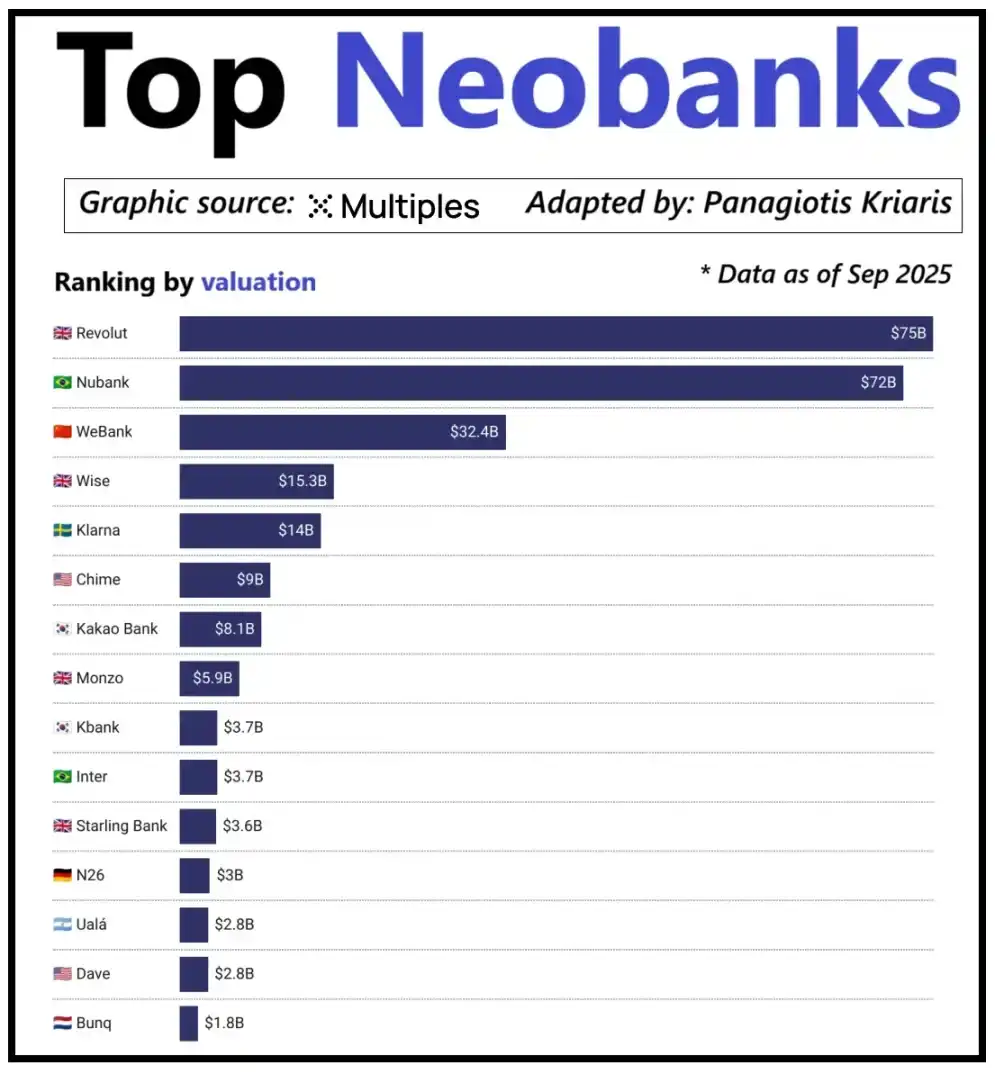

Looking at the top digital banks globally, their valuation is not simply determined by user scale but by their ability to generate revenue per user. Digital bank Revolut is a prime example: despite having fewer users than Brazilian digital bank Nubank, its valuation surpasses the latter. The reason lies in Revolut's diversified revenue streams, covering areas such as foreign exchange trading, securities trading, wealth management, and premium membership services. In contrast, Nubank's business expansion relies mainly on credit operations and interest income rather than bank card fees. China's WeBank has taken a different path of differentiation, achieving growth through extreme cost control and deep integration into the Tencent ecosystem.

Valuation of Top Emerging Digital Banks

Currently, crypto digital banks are experiencing a similar development milestone. The combination of "wallet + bank card" can no longer be called a business model, as any institution can easily launch such services. The platform's competitive advantage lies precisely in its chosen core monetization path: some platforms earn interest income from user account balances, some rely on stablecoin transaction volume for profits, and a few platforms place their growth potential in stablecoin issuance and management, as this is the most stable and predictable source of income in the market.

This also explains why the importance of the stablecoin race is becoming increasingly prominent. For reserve-backed stablecoins, their core profit comes from investment returns on reserves, i.e., the interest generated by investing reserves in short-term government bonds or cash equivalents. This income belongs to the stablecoin issuer rather than just the digital bank providing stablecoin holding and spending functions to users. This profit model is not unique to the crypto industry: in the traditional financial sector, digital banks also cannot earn interest from user deposits, and the actual custodian banks holding the funds enjoy this income. With the emergence of stablecoins, this "separation of income ownership" model has become more transparent and centralized, where entities holding short-term government bonds and cash equivalents earn interest income, while consumer-facing applications are primarily responsible for user acquisition and product experience optimization.

As the adoption of stablecoins continues to grow, a contradiction is gradually emerging: application platforms that undertake user acquisition, transaction matching, and trust building often cannot profit from the underlying reserve. This value gap is forcing enterprises to integrate into vertical domains, moving away from a mere frontend tool positioning towards the core of fund custody and management.

It is precisely due to this consideration that companies like Stripe and Circle have been increasing their efforts to lay out their strategies in the stablecoin ecosystem. They are no longer satisfied with staying at the distribution level but are expanding into the settlement and reserve management field, as this is the core profit-making area of the entire system. For example, Stripe launched its dedicated blockchain called Tempo, specifically designed for low-cost, instant transfers of stablecoins. Stripe did not rely on existing public blockchains like Ethereum or Solana but built its own transaction channels to control the settlement process, fee pricing, and transaction throughput, all of which directly translate into better economic benefits.

Circle has also adopted a similar strategy by creating a dedicated settlement network called Arc for USDC. Through Arc, inter-institution USDC transfers can be completed in real-time without causing congestion on the public chain network, nor incurring high fees. Essentially, Circle has built an independent USDC backend system through Arc, no longer being dependent on external infrastructure.

Privacy protection is another important driver of this strategy. As Prathik elaborated in the article "Reshaping the Brilliance of Blockchain," a public blockchain records every stablecoin transfer on a publicly transparent ledger. This feature is suitable for an open financial system but has drawbacks in commercial scenarios such as salary payments, supplier payments, and treasury management. In these scenarios, transaction amounts, counterparties, and payment patterns are sensitive information.

In practice, the high transparency of public chains allows third parties to easily reconstruct a company's internal financial situation through blockchain explorers and on-chain analysis tools. The Arc network enables inter-institution USDC transfers to settle outside of the public chain, preserving the advantage of fast stablecoin settlement while ensuring the confidentiality of transaction information.

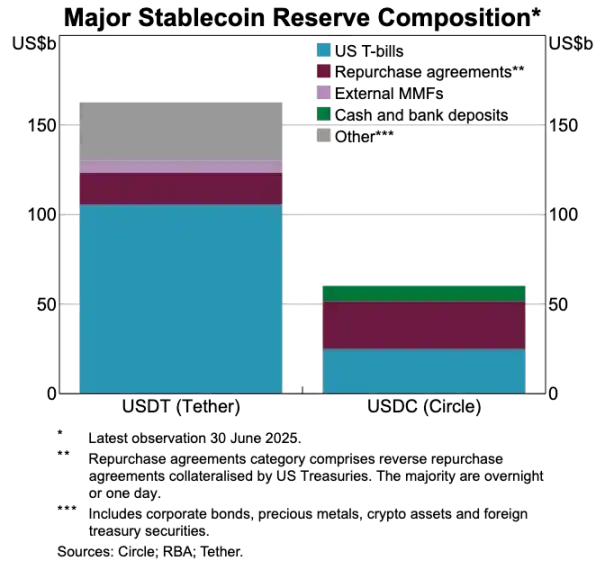

Comparison of USDT and USDC Asset Reserves

Stablecoins Are Disrupting the Old Payment System

If stablecoins are at the core of value, the traditional payment system appears increasingly outdated. The current payment process involves multiple intermediaries: the receiving gateway is responsible for fund collection, the payment processor completes transaction routing, card networks authorize transactions, and the account-holding banks of the transaction parties ultimately settle. Each step incurs costs and causes transaction delays.

Stablecoins, on the other hand, bypass this lengthy chain of intermediaries. Stablecoin transactions do not require card networks or acquirers and do not need to wait for batch settlement windows. Instead, they are based on the underlying network to facilitate direct peer-to-peer transfers. This feature has a profound impact on digital banks, as it completely changes users' experience expectations. If users can achieve instant fund transfers on other platforms, they will not tolerate the cumbersome and costly transfer processes within digital banks. Digital banks either need to deeply integrate stablecoin transaction channels or risk becoming the least efficient part of the entire payment chain.

This transformation also reshapes the business model of digital banks. In the traditional system, digital banks could earn stable fee income through bank card transactions because the payment network firmly controlled the core of transaction flow. However, in the new system dominated by stablecoins, this profit margin has been greatly compressed. Since stablecoin peer-to-peer transfers do not have transaction fees, digital banks relying solely on bank card spending for revenue are facing a completely fee-less competitive track.

Therefore, the role of digital banks is shifting from card issuers to payment routing layers. As payment methods shift from bank cards to stablecoin direct transfers, digital banks must become the core circulation nodes of stablecoin transactions. Digital banks that can efficiently process stablecoin transaction flows will dominate the market because once users see them as the default channel for fund transfers, it is challenging to switch to other platforms.

Identity Authentication is Becoming the New Generation Account Carrier

As stablecoins make payments faster and cheaper, another equally important bottleneck is gradually emerging: identity authentication. In the traditional financial system, identity authentication is a separate process: banks collect user documents, store information, and conduct verifications in the background. However, in the scenario of instant wallet fund transfers, every transaction relies on a trusted identity authentication system. Without this system, compliance checks, anti-fraud controls, and even basic permission management are not possible.

For this reason, identity authentication and payment functionality are rapidly converging. The market is gradually moving away from separate KYC processes on each platform and shifting towards a portable identity authentication system that can be used across services, countries, and platforms.

This transformation is unfolding in Europe, where the EU digital identity wallet has entered the implementation phase. The EU no longer requires each bank or application to independently conduct identity verification; instead, it has created a government-endorsed unified identity wallet that all residents and businesses can use. This wallet is used not only for identity storage but also carries various authenticated credentials (such as age, residency proof, licensing qualifications, tax information, etc.), supports users in signing electronic documents, and has built-in payment functions. Users can complete identity verification, share information on demand, and payment operations in a single process, achieving full-process seamless integration.

If the EU Digital Identity Wallet is successfully implemented, the entire European banking architecture will be restructured: Identity authentication will replace bank accounts as the core entry point for financial services. This will make identity authentication a public good, and the distinction between traditional banks and digital banks will be weakened, unless they can develop value-added services based on this trusted identity system.

The crypto industry is also evolving in the same direction. Experiments related to on-chain identity authentication have been conducted for many years. Although there is currently no perfect solution, all explorations point to the same goal: to provide users with a means of identity verification that allows them to prove their identity or relevant facts without limiting the information to a single platform.

Here are several typical examples:

· Worldcoin: Building a global-scale identity proof system that verifies users' real human identity without revealing their privacy.

· Gitcoin Passport: Integrating various credentials and verifications to reduce the risk of sybil attacks in governance voting and reward distribution processes.

· Polygon ID, zkPass, and ZK-proof frameworks: Supporting users in proving specific facts without revealing underlying data.

· Ethereum Name Service (ENS) + off-chain credentials: Allowing crypto wallets to not only display asset balances but also associate users' social identities and authentication attributes.

The goal of most crypto identity authentication projects is consistent: to enable users to autonomously prove their identity or relevant facts, and ensure that identity information is not locked into a single platform. This aligns with the EU's vision of a digital identity wallet: an identity credential that can freely flow between different applications with no need for revalidation.

This trend will also transform the operating model of digital banks. Today, digital banks see identity authentication as a core control mechanism: user registration, platform audits, ultimately forming an account subordinate to the platform. However, when identity authentication becomes a credential that users can autonomously carry, the role of digital banks shifts to being a service provider accessing this trusted identity system. This will simplify the user onboarding process, reduce compliance costs, minimize redundant verification, and allow crypto wallets to replace bank accounts as the core vessel for user assets and identity.

Future Development Trends Outlook

In conclusion, the former core elements of the digital banking system are gradually losing their competitive edge: user scale is no longer a moat, bank cards are no longer a moat, and even a streamlined user interface is no longer a moat. The real differentiation competitive barriers are reflected in three dimensions: the profit products chosen by digital banks, the fund flow channels they rely on, and the identity authentication system they access. Apart from these, other functions will gradually converge, and substitutability will become stronger.

The future successful digital banks will not be lightweight versions of traditional banks, but rather wallet-first financial systems. They will anchor on a core profit engine, which directly determines the platform's profit margin and competitive moat. Overall, the core profit engine can be divided into three categories:

Interest-Driven Digital Bank

The core competitiveness of these platforms is to become the preferred channel for users to hold stablecoins. As long as they can attract a large number of user balances, the platform can earn income through reserve-backed stablecoin interest, on-chain rewards, staking, and re-staking, without relying on a large user base. The advantage lies in the fact that the profit efficiency of asset holding is much higher than that of asset circulation. These digital banks may seem like consumer-facing applications, but they are actually modern savings platforms disguised as wallets, with the core competitiveness of providing users with a seamless interest-earning experience.

Payment Flow-Driven Digital Bank

The value proposition of these platforms comes from transaction volume. They will become the primary channel for users to send and receive stablecoin payments, and for consumption, deeply integrating payment processing, merchants, fiat-to-crypto exchanges, and cross-border payment channels. Their profit model is similar to that of global payment giants—thin profit margins per transaction, but once they become the user's preferred fund transfer channel, they can accumulate substantial income through a large transaction volume. Their moat is user habits and service reliability, becoming the default choice when users need to transfer funds.

Stablecoin Infrastructure-Driven Digital Bank

This is the deepest and potentially highest-reward track. These digital banks are not just channels for stablecoin circulation but are dedicated to controlling the issuance of stablecoins, or at least controlling their underlying infrastructure, with business scopes covering stablecoin issuance, redemption, reserve management, and settlement, among other core processes. The profit potential in this field is the most lucrative because control over the reserve directly determines income attribution. These digital banks integrate consumer-side functions with infrastructure ambitions, evolving towards a full-fledged financial network rather than just applications.

In short, Interest-Driven Digital Banks make money from user deposits, Payment Flow-Driven Digital Banks make money from user transactions, and Infrastructure-Driven Digital Banks can generate continuous profits regardless of user actions.

I anticipate that the market will diverge into two major camps: the first camp consists of consumer-facing application platforms that mainly integrate existing infrastructure, offer simple and user-friendly products, but have extremely low user conversion costs. The second camp moves towards the core area of value aggregation, focusing on stablecoin issuance, transaction routing, settlement, and identity verification integration, among other businesses.

The latter's positioning will no longer be limited to applications but as infrastructure service providers disguised in consumer-facing attire. Their user stickiness is extremely high as they quietly become the core systems for on-chain fund circulation.

You may also like

1 billion DOTs were minted out of thin air, but the hacker only made 230,000 dollars

After the blockade of the Strait of Hormuz, when will the war end?

Before using Musk's "Western WeChat" X Chat, you need to understand these three questions

The X Chat will be available for download on the App Store this Friday. The media has already covered the feature list, including self-destructing messages, screenshot prevention, 481-person group chats, Grok integration, and registration without a phone number, positioning it as the "Western WeChat." However, there are three questions that have hardly been addressed in any reports.

There is a sentence on X's official help page that is still hanging there: "If malicious insiders or X itself cause encrypted conversations to be exposed through legal processes, both the sender and receiver will be completely unaware."

No. The difference lies in where the keys are stored.

In Signal's end-to-end encryption, the keys never leave your device. X, the court, or any external party does not hold your keys. Signal's servers have nothing to decrypt your messages; even if they were subpoenaed, they could only provide registration timestamps and last connection times, as evidenced by past subpoena records.

X Chat uses the Juicebox protocol. This solution divides the key into three parts, each stored on three servers operated by X. When recovering the key with a PIN code, the system retrieves these three shards from X's servers and recombines them. No matter how complex the PIN code is, X is the actual custodian of the key, not the user.

This is the technical background of the "help page sentence": because the key is on X's servers, X has the ability to respond to legal processes without the user's knowledge. Signal does not have this capability, not because of policy, but because it simply does not have the key.

The following illustration compares the security mechanisms of Signal, WhatsApp, Telegram, and X Chat along six dimensions. X Chat is the only one of the four where the platform holds the key and the only one without Forward Secrecy.

The significance of Forward Secrecy is that even if a key is compromised at a certain point in time, historical messages cannot be decrypted because each message has a unique key. Signal's Double Ratchet protocol automatically updates the key after each message, a mechanism lacking in X Chat.

After analyzing the X Chat architecture in June 2025, Johns Hopkins University cryptology professor Matthew Green commented, "If we judge XChat as an end-to-end encryption scheme, this seems like a pretty game-over type of vulnerability." He later added, "I would not trust this any more than I trust current unencrypted DMs."

From a September 2025 TechCrunch report to being live in April 2026, this architecture saw no changes.

In a February 9, 2026 tweet, Musk pledged to undergo rigorous security tests of X Chat before its launch on X Chat and to open source all the code.

As of the April 17 launch date, no independent third-party audit has been completed, there is no official code repository on GitHub, the App Store's privacy label reveals X Chat collects five or more categories of data including location, contact info, and search history, directly contradicting the marketing claim of "No Ads, No Trackers."

Not continuous monitoring, but a clear access point.

For every message on X Chat, users can long-press and select "Ask Grok." When this button is clicked, the message is delivered to Grok in plaintext, transitioning from encrypted to unencrypted at this stage.

This design is not a vulnerability but a feature. However, X Chat's privacy policy does not state whether this plaintext data will be used for Grok's model training or if Grok will store this conversation content. By actively clicking "Ask Grok," users are voluntarily removing the encryption protection of that message.

There is also a structural issue: How quickly will this button shift from an "optional feature" to a "default habit"? The higher the quality of Grok's replies, the more frequently users will rely on it, leading to an increase in the proportion of messages flowing out of encryption protection. The actual encryption strength of X Chat, in the long run, depends not only on the design of the Juicebox protocol but also on the frequency of user clicks on "Ask Grok."

X Chat's initial release only supports iOS, with the Android version simply stating "coming soon" without a timeline.

In the global smartphone market, Android holds about 73%, while iOS holds about 27% (IDC/Statista, 2025). Of WhatsApp's 3.14 billion monthly active users, 73% are on Android (according to Demand Sage). In India, WhatsApp covers 854 million users, with over 95% Android penetration. In Brazil, there are 148 million users, with 81% on Android, and in Indonesia, there are 112 million users, with 87% on Android.

WhatsApp's dominance in the global communication market is built on Android. Signal, with a monthly active user base of around 85 million, also relies mainly on privacy-conscious users in Android-dominant countries.

X Chat circumvented this battlefield, with two possible interpretations. One is technical debt; X Chat is built with Rust, and achieving cross-platform support is not easy, so prioritizing iOS may be an engineering constraint. The other is a strategic choice; with iOS holding a market share of nearly 55% in the U.S., X's core user base being in the U.S., prioritizing iOS means focusing on their core user base rather than engaging in direct competition with Android-dominated emerging markets and WhatsApp.

These two interpretations are not mutually exclusive, leading to the same result: X Chat's debut saw it willingly forfeit 73% of the global smartphone user base.

This matter has been described by some: X Chat, along with X Money and Grok, forms a trifecta creating a closed-loop data system parallel to the existing infrastructure, similar in concept to the WeChat ecosystem. This assessment is not new, but with X Chat's launch, it's worth revisiting the schematic.

X Chat generates communication metadata, including information on who is talking to whom, for how long, and how frequently. This data flows into X's identity system. Part of the message content goes through the Ask Grok feature and enters Grok's processing chain. Financial transactions are handled by X Money: external public testing was completed in March, opening to the public in April, enabling fiat peer-to-peer transfers via Visa Direct. A senior Fireblocks executive confirmed plans for cryptocurrency payments to go live by the end of the year, holding money transmitter licenses in over 40 U.S. states currently.

Every WeChat feature operates within China's regulatory framework. Musk's system operates within Western regulatory frameworks, but he also serves as the head of the Department of Government Efficiency (DOGE). This is not a WeChat replica; it is a reenactment of the same logic under different political conditions.

The difference is that WeChat has never explicitly claimed to be "end-to-end encrypted" on its main interface, whereas X Chat does. "End-to-end encryption" in user perception means that no one, not even the platform, can see your messages. X Chat's architectural design does not meet this user expectation, but it uses this term.

X Chat consolidates the three data lines of "who this person is, who they are talking to, and where their money comes from and goes to" in one company's hands.

The help page sentence has never been just technical instructions.

Parse Noise's newly launched Beta version, how to "on-chain" this heat?

Is Lobster a Thing of the Past? Unpacking the Hermes Agent Tools that Supercharge Your Throughput to 100x

Declare War on AI? The Doomsday Narrative Behind Ultraman's Residence in Flames

Crypto VCs Are Dead? The Market Extinction Cycle Has Begun

Claude's Journey to Foolishness in Diagrams: The Cost of Thriftiness, or How API Bill Increased 100-Fold

Edge Land Regress: A Rehash Around Maritime Power, Energy, and the Dollar

Arthur Hayes Latest Interview: How Should Retail Investors Navigate the Iran Conflict?

Just now, Sam Altman was attacked again, this time by gunfire

Straits Blockade, Stablecoin Recap | Rewire News Morning Edition

From High Expectations to Controversial Turnaround, Genius Airdrop Triggers Community Backlash

The Xiaomi electric vehicle factory in Beijing's Daxing district has become the new Jerusalem for the American elite

Lean Harness, Fat Skill: The Real Source of 100x AI Productivity

Ultraman is not afraid of his mansion being attacked; he has a fortress.

US-Iran Negotiations Collapse, Bitcoin Faces Battle to Defend $70,000 Level

Reflections and Confusions of a Crypto VC

1 billion DOTs were minted out of thin air, but the hacker only made 230,000 dollars

After the blockade of the Strait of Hormuz, when will the war end?

Before using Musk's "Western WeChat" X Chat, you need to understand these three questions

The X Chat will be available for download on the App Store this Friday. The media has already covered the feature list, including self-destructing messages, screenshot prevention, 481-person group chats, Grok integration, and registration without a phone number, positioning it as the "Western WeChat." However, there are three questions that have hardly been addressed in any reports.

There is a sentence on X's official help page that is still hanging there: "If malicious insiders or X itself cause encrypted conversations to be exposed through legal processes, both the sender and receiver will be completely unaware."

No. The difference lies in where the keys are stored.

In Signal's end-to-end encryption, the keys never leave your device. X, the court, or any external party does not hold your keys. Signal's servers have nothing to decrypt your messages; even if they were subpoenaed, they could only provide registration timestamps and last connection times, as evidenced by past subpoena records.

X Chat uses the Juicebox protocol. This solution divides the key into three parts, each stored on three servers operated by X. When recovering the key with a PIN code, the system retrieves these three shards from X's servers and recombines them. No matter how complex the PIN code is, X is the actual custodian of the key, not the user.

This is the technical background of the "help page sentence": because the key is on X's servers, X has the ability to respond to legal processes without the user's knowledge. Signal does not have this capability, not because of policy, but because it simply does not have the key.

The following illustration compares the security mechanisms of Signal, WhatsApp, Telegram, and X Chat along six dimensions. X Chat is the only one of the four where the platform holds the key and the only one without Forward Secrecy.

The significance of Forward Secrecy is that even if a key is compromised at a certain point in time, historical messages cannot be decrypted because each message has a unique key. Signal's Double Ratchet protocol automatically updates the key after each message, a mechanism lacking in X Chat.

After analyzing the X Chat architecture in June 2025, Johns Hopkins University cryptology professor Matthew Green commented, "If we judge XChat as an end-to-end encryption scheme, this seems like a pretty game-over type of vulnerability." He later added, "I would not trust this any more than I trust current unencrypted DMs."

From a September 2025 TechCrunch report to being live in April 2026, this architecture saw no changes.

In a February 9, 2026 tweet, Musk pledged to undergo rigorous security tests of X Chat before its launch on X Chat and to open source all the code.

As of the April 17 launch date, no independent third-party audit has been completed, there is no official code repository on GitHub, the App Store's privacy label reveals X Chat collects five or more categories of data including location, contact info, and search history, directly contradicting the marketing claim of "No Ads, No Trackers."

Not continuous monitoring, but a clear access point.

For every message on X Chat, users can long-press and select "Ask Grok." When this button is clicked, the message is delivered to Grok in plaintext, transitioning from encrypted to unencrypted at this stage.

This design is not a vulnerability but a feature. However, X Chat's privacy policy does not state whether this plaintext data will be used for Grok's model training or if Grok will store this conversation content. By actively clicking "Ask Grok," users are voluntarily removing the encryption protection of that message.

There is also a structural issue: How quickly will this button shift from an "optional feature" to a "default habit"? The higher the quality of Grok's replies, the more frequently users will rely on it, leading to an increase in the proportion of messages flowing out of encryption protection. The actual encryption strength of X Chat, in the long run, depends not only on the design of the Juicebox protocol but also on the frequency of user clicks on "Ask Grok."

X Chat's initial release only supports iOS, with the Android version simply stating "coming soon" without a timeline.

In the global smartphone market, Android holds about 73%, while iOS holds about 27% (IDC/Statista, 2025). Of WhatsApp's 3.14 billion monthly active users, 73% are on Android (according to Demand Sage). In India, WhatsApp covers 854 million users, with over 95% Android penetration. In Brazil, there are 148 million users, with 81% on Android, and in Indonesia, there are 112 million users, with 87% on Android.

WhatsApp's dominance in the global communication market is built on Android. Signal, with a monthly active user base of around 85 million, also relies mainly on privacy-conscious users in Android-dominant countries.

X Chat circumvented this battlefield, with two possible interpretations. One is technical debt; X Chat is built with Rust, and achieving cross-platform support is not easy, so prioritizing iOS may be an engineering constraint. The other is a strategic choice; with iOS holding a market share of nearly 55% in the U.S., X's core user base being in the U.S., prioritizing iOS means focusing on their core user base rather than engaging in direct competition with Android-dominated emerging markets and WhatsApp.

These two interpretations are not mutually exclusive, leading to the same result: X Chat's debut saw it willingly forfeit 73% of the global smartphone user base.

This matter has been described by some: X Chat, along with X Money and Grok, forms a trifecta creating a closed-loop data system parallel to the existing infrastructure, similar in concept to the WeChat ecosystem. This assessment is not new, but with X Chat's launch, it's worth revisiting the schematic.

X Chat generates communication metadata, including information on who is talking to whom, for how long, and how frequently. This data flows into X's identity system. Part of the message content goes through the Ask Grok feature and enters Grok's processing chain. Financial transactions are handled by X Money: external public testing was completed in March, opening to the public in April, enabling fiat peer-to-peer transfers via Visa Direct. A senior Fireblocks executive confirmed plans for cryptocurrency payments to go live by the end of the year, holding money transmitter licenses in over 40 U.S. states currently.

Every WeChat feature operates within China's regulatory framework. Musk's system operates within Western regulatory frameworks, but he also serves as the head of the Department of Government Efficiency (DOGE). This is not a WeChat replica; it is a reenactment of the same logic under different political conditions.

The difference is that WeChat has never explicitly claimed to be "end-to-end encrypted" on its main interface, whereas X Chat does. "End-to-end encryption" in user perception means that no one, not even the platform, can see your messages. X Chat's architectural design does not meet this user expectation, but it uses this term.

X Chat consolidates the three data lines of "who this person is, who they are talking to, and where their money comes from and goes to" in one company's hands.

The help page sentence has never been just technical instructions.