Buy Crypto

Buy Crypto- Markets

Futures

Futures- Spot

- Copy Trade

- Earn

- More

Three Charts to Watch at NVIDIA's GTC: Cheaper Compute, Spend More

Last night, Huang Renxun announced the Vera Rubin platform at GTC 2026, claiming that the power consumption per inference performance is 10 times higher than Blackwell, the cost per inference Token has been reduced to one-tenth, and hinted that the merger order between Blackwell and Vera Rubin will exceed $1 trillion by 2027.

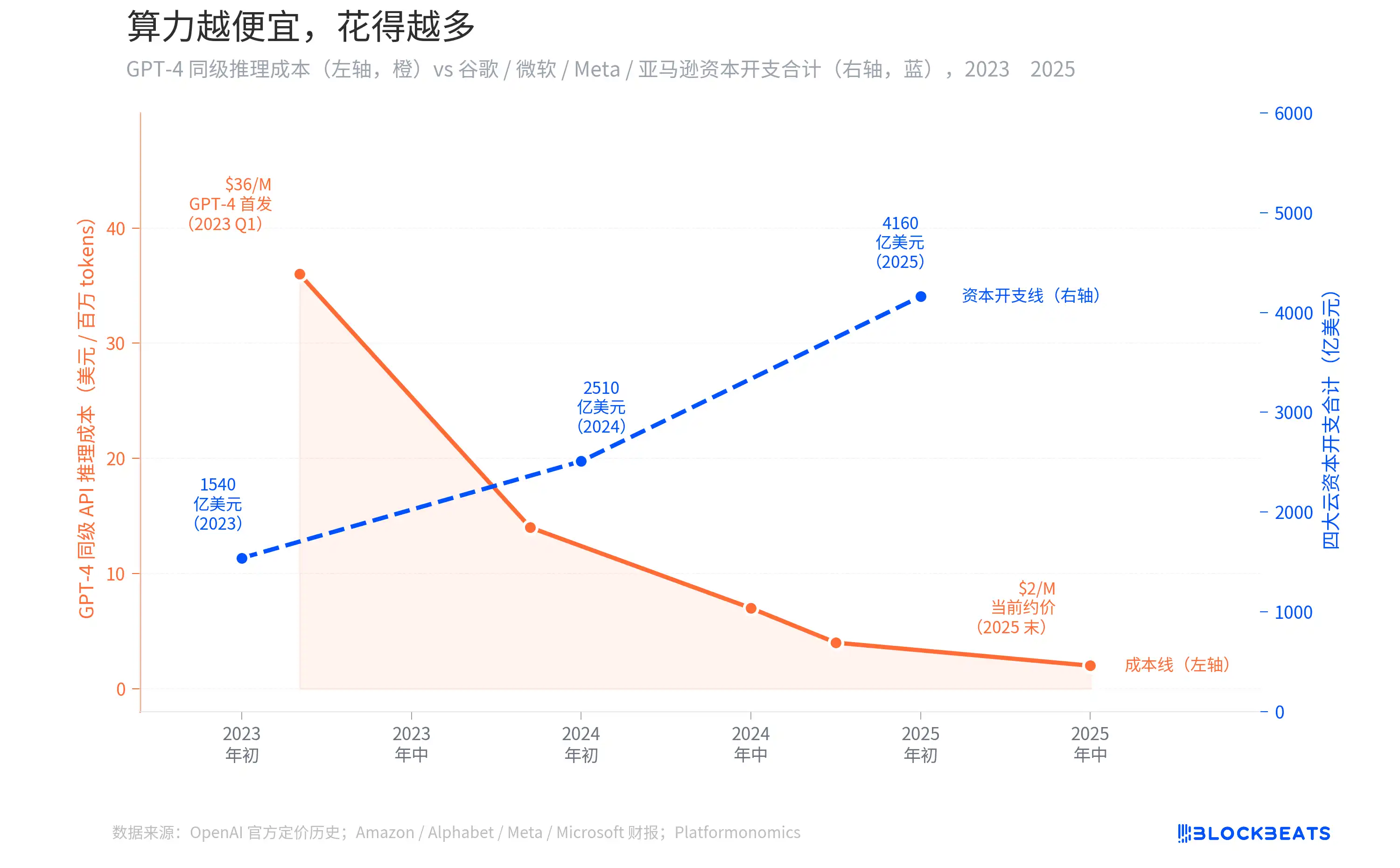

Over the past two years, the inference cost of GPT-4-level APIs has plummeted by 94%, from $36 per million Tokens to less than $2. Intuitively, with the decrease in computing costs, businesses should be spending less. However, the combined capital expenditures of the four cloud providers Amazon, Alphabet, Meta, and Microsoft have increased from $154 billion to $416 billion, nearly tripling.

Huang Renxun's trillion-dollar hint is not just a marketing slogan; it is backed by a curve that can be drawn with data.

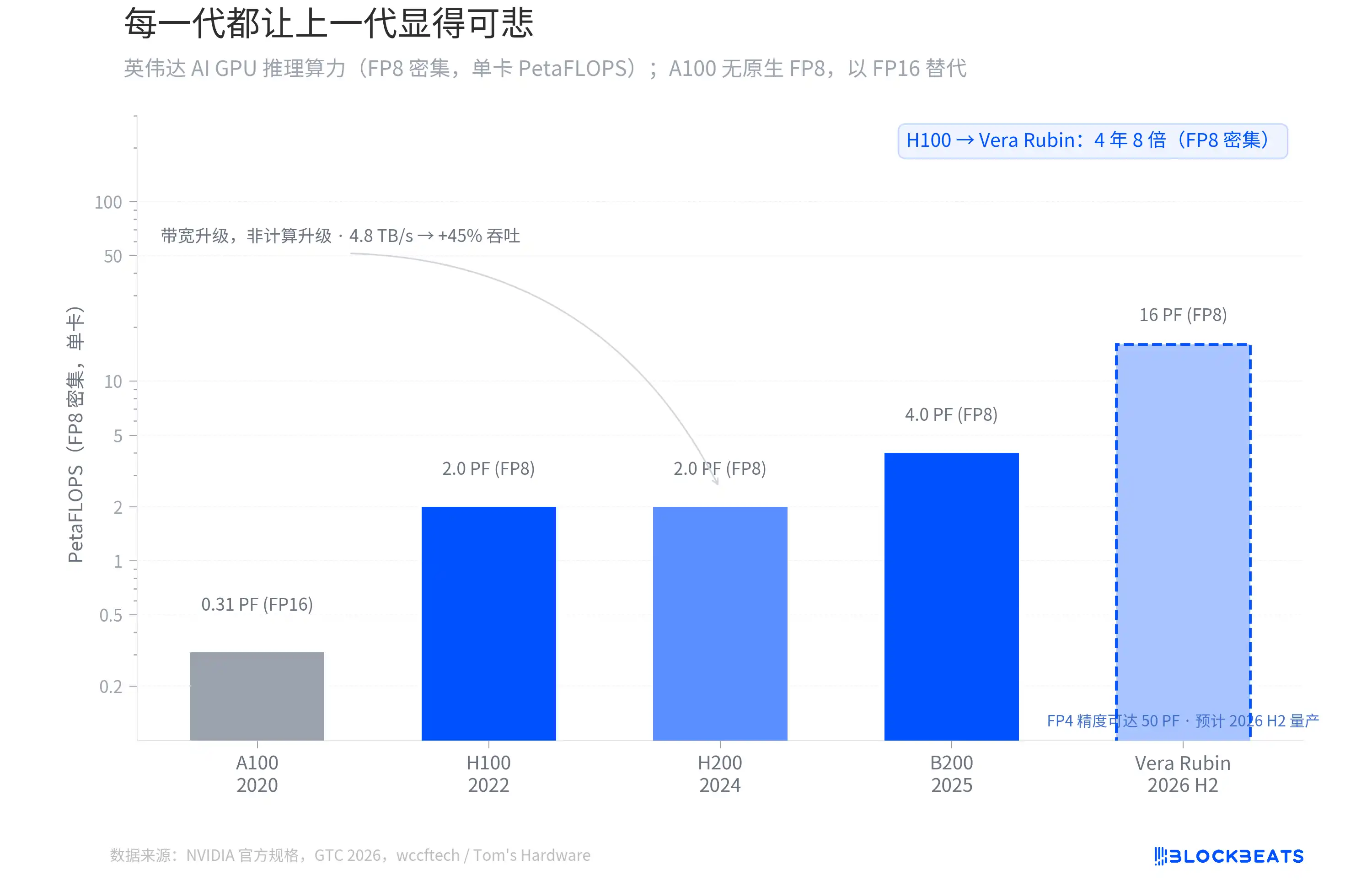

Each Generation Makes the Previous Generation Seem Pathetic

From the H100 of 2022 to the Vera Rubin set to be mass-produced in the second half of 2026, NVIDIA's AI GPU FP8 dense inference computing power has increased 8-fold in four years. According to NVIDIA's official specifications, the H100 single card has 2.0 PetaFLOPS, the B200 reaches 4.0 PF, and the Vera Rubin directly jumps to 16 PF.

However, not every generational leap comes from the same place. According to wccftech, the H200's computing cores are identical to the H100, with no change in FP8 computing power; all its upgrades come from memory bandwidth (increased from 3.35 TB/s to 4.8 TB/s), bringing about a roughly 45% inference throughput increase.

The real architectural transition occurred between B200 and Vera Rubin. Vera Rubin adopts TSMC's 3nm process, featuring a dual-chiplet design with 336B transistors, achieving 50 PF of computing power at FP4 precision. According to Tom's Hardware, the first Vera Rubin system is already running on Microsoft Azure.

There is a subtle distinction that is easy to overlook. When Huang Renxun mentioned "10 times" at GTC, he was referring to the reduction in Token cost per inference, not a multiple of the original computing power. The Token cost includes Transformer Engine optimization, FP4 precision, larger batch inference, and other system-level factors. Looking at standardized FP8 dense TFLOPS, Vera Rubin is 4 times greater than Blackwell and 8 times greater than H100.

The slope of this curve has never slowed down. Each generation of GPUs has made the previous generation look inadequate, and that is exactly the starting point of the story to be told next.

Jevons Paradox: The cheaper the computational power, the more is spent

In March 2023, when GPT-4 was just launched, the API call cost was about $36 per million Tokens. According to OpenAI's official pricing history, by the mid of 2024 with the introduction of GPT-4o, it dropped to around $7, and by the end of 2025, the actual available price had fallen below $2. A decrease of over 94% in two years.

Logically, with inference costs dropping so much, businesses should spend less. However, the reality is quite the opposite. According to various company's financial reports and data tracked by Platformonomics, the combined annual capital expenditure of the four cloud providers Amazon, Alphabet, Meta, Microsoft increased from $154 billion in 2023 to $416 billion in 2025, a growth of 170%. Google alone surged from $32 billion to $91.5 billion (about 2.9 times), with Microsoft's increase even greater.

This phenomenon has a name in economics, called the Jevons Paradox. In 1865, the British economist William Jevons found that Watt's improvements to the steam engine significantly increased the efficiency of coal use, but the coal consumption in the UK did not decrease; instead, it rose. The reason is simple: the efficiency improvement made the steam engine more cost-effective, so more industries started using steam engines, and total demand expanded far beyond the part saved by efficiency.

Today, the situation with AI inference is exactly the same. As API prices plummeted to 6% of their original, enterprises did not save budget because of it but started fitting AI into previously uneconomical scenarios. Every new scenario like customer service, code review, content generation, search reordering, ad bidding is consuming more inference power. The expansion of demand far exceeds the rate of cost decline. In early 2025, DeepSeek R1 pushed the input price to $0.55 per million Tokens, further accelerating this cycle. The two lines moving in opposite directions on the chart represent two sides of the same coin.

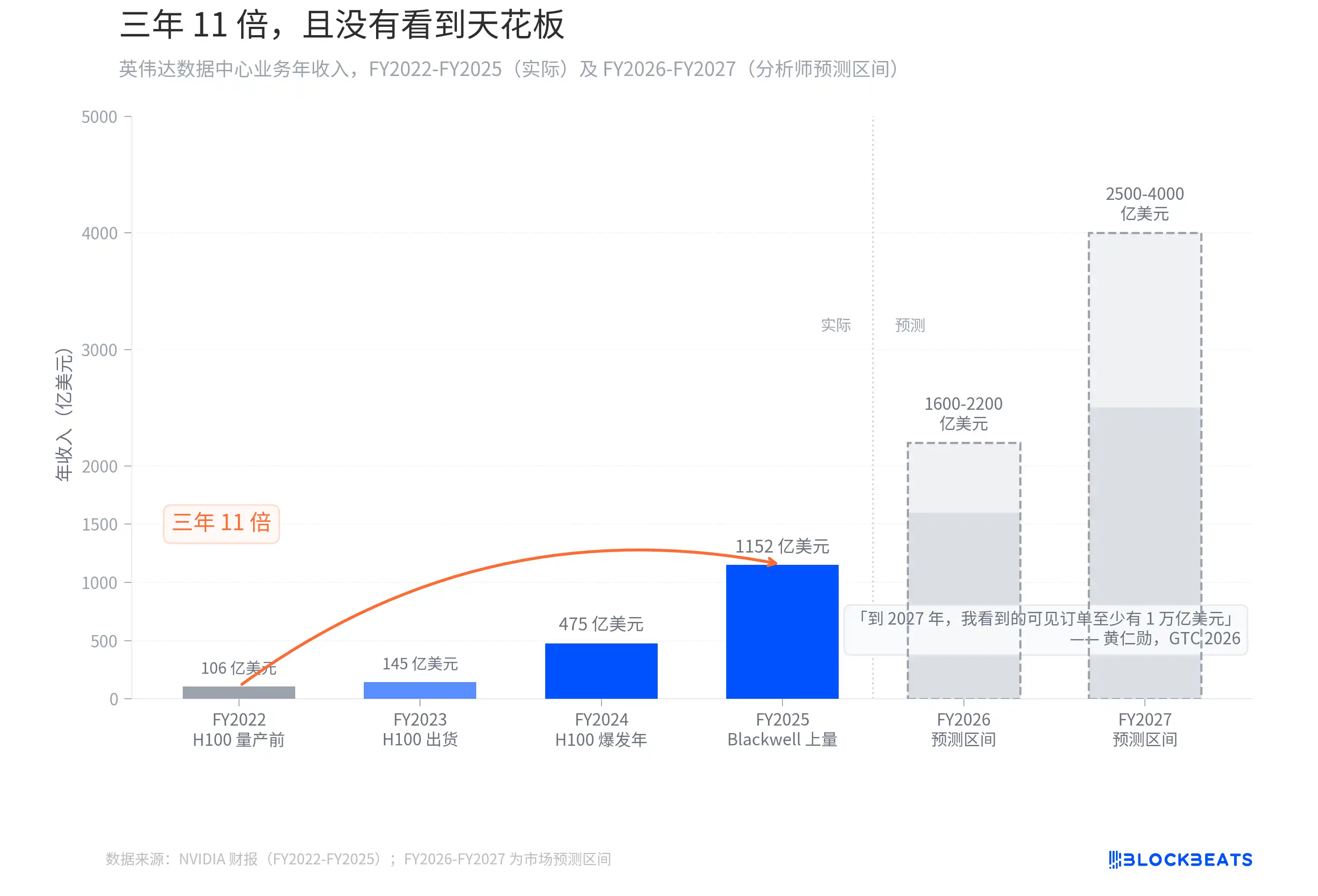

Three years, an 11-fold increase, and no sight of a ceiling

If the Jevons Paradox has a most direct beneficiary, it is the one selling shovels.

According to NVIDIA's financial report, the data center business's annual revenue increased from $10.6 billion in FY2022 (ending January 2022) to $115.2 billion in FY2025 (ending January 2025), a growth of 10.9x over three fiscal years. This growth curve has almost no precedent in tech history. For comparison, after the iPhone was launched in 2007, it took Apple about 6 years to achieve a similar order of magnitude revenue scale increase.

Then, Jensen Huang said at GTC 2026, "By 2027, the visible orders that I see are at least $1 trillion. In fact, our capacity will not be enough. I am confident that the computing demand will far exceed this number."

His forecast last year at GTC was around $500 billion in visible orders by 2026. A year later, the number doubled, with the time window extended by just one year. Analysts' revenue forecasts for FY2026-FY2027 range between $160-220 billion and $250-400 billion, respectively. However, Huang himself stated that this number is not a ceiling, "the computing demand will far exceed this number." On the day GTC ended, NVIDIA's stock price rose by 4.3%. The market evidently chose to believe him.

Each generation of GPU makes the previous look pitiful, and each round of price cuts makes the next round of capital expenditure seem natural. NVIDIA is currently situated in the sweetest spot of this paradox.

You may also like

US AI Startup Goes All In on Chinese Mega-Model | Rewire News Morning Brief

Trump Lies Again: A "Five-Day Pause" Psyop, How Wall Street, Bitcoin, and Polymarket Insiders Synced Uposciogen

When a Token Becomes Labor, People Become the Interface

Ceasefire News Leaked Ahead of Time? Large Polymarket Bets on Outcome Before Trump's Tweet

BlackRock CEO's Annual Shareholder Letter: How is Wall Street Using AI to Keep Profiting from National Pension Funds?

Sun Valley Releases 2025 Financial Report: Bitcoin Mining Revenue Reaches $670 Million, Accelerating Transformation to AI Infrastructure Platform

On March 16, 2026, in Dallas, Texas, USA, CanGu Company (New York Stock Exchange code: CANG, hereinafter referred to as "CanGu" or the "Company") today announced its unaudited financial performance for the fourth quarter and full year ended December 31, 2025. As a bitcoin mining enterprise relying on a globally operated layout and dedicated to building an integrated energy and AI computing power platform, CanGu is actively advancing its business transformation and infrastructure development.

• Financial Performance:

Total revenue for the full year 2025 was $688.1 million, with $179.5 million in the fourth quarter.

Bitcoin mining business revenue for the full year was $675.5 million, with $172.4 million in the fourth quarter.

Full-year adjusted EBITDA was $24.5 million, while the fourth quarter was -$156.3 million.

• Mining Operations and Costs:

A total of 6,594.6 bitcoins were mined throughout the year, averaging 18.07 bitcoins per day; of which 1,718.3 bitcoins were mined in the fourth quarter, averaging 18.68 bitcoins per day.

The average mining cost for the full year (excluding miner depreciation) was $79,707 per bitcoin, and for the fourth quarter, it was $84,552;

The all-in sustaining costs were $97,272 and $106,251 per bitcoin, respectively.

As of the end of December 2025, the company has cumulatively produced 7,528.4 bitcoins since entering the bitcoin mining business.

• Strategic Progress:

The company has completed the termination of the American Depositary Receipt (ADR) program and transitioned to a direct listing on the NYSE to enhance information transparency and align with its strategic direction, with a long-term goal of expanding its investor base.

CEO Paul Yu stated: "2025 marked the company's first full year as a bitcoin mining enterprise, characterized by rapid execution and structural reshaping. We completed a comprehensive adjustment of our asset system and established a globally distributed mining network. Additionally, the company introduced a new management team, further strengthening our capabilities and competitive advantage in the digital asset and energy infrastructure space. The completion of the NYSE direct listing and USD pricing also signifies our transformation into a global AI infrastructure company."

"As we enter 2026, the company will continue to optimize its balance sheet structure and enhance operational efficiency and cost resilience through adjustments to the miner portfolio. At the same time, we are advancing our strategic transformation into an AI infrastructure provider. Leveraging EcoHash, we will utilize our capabilities in scalable computing power and energy networks to provide cost-effective AI inference solutions. The relevant site transformations and product development are progressing simultaneously, and the company is well-positioned to sustain its execution in the new phase."

The company's Chief Financial Officer, Michael Zhang, stated: "By 2025, the company is expected to achieve significant revenue growth through its scaled mining operations. Despite recording a net loss of $452.8 million from ongoing operations, mainly due to one-time transformation costs and market-driven fair value adjustments, the company, from a financial perspective, will reduce its leverage, optimize its Bitcoin reserve strategy and liquidity management, introduce new capital to strengthen its financial position, and seize investment opportunities in high-potential areas such as AI infrastructure while navigating market volatility."

The total revenue for the fourth quarter was $1.795 billion. Of this, the Bitcoin mining business contributed $1.724 billion in revenue, generating 1,718.3 Bitcoins during the quarter. Revenue from the international automobile trading business was $4.8 million.

The total operating costs and expenses for the fourth quarter amounted to $4.56 billion, primarily attributed to expenses related to the Bitcoin mining business, as well as impairment of mining machines and fair value losses on Bitcoin collateral receivables.

This includes:

· Cost of Revenue (excluding depreciation): $1.553 billion

· Cost of Revenue (depreciation): $38.1 million

· Operating Expenses: $9.9 million (including related-party expenses of $1.1 million)

· Mining Machine Impairment Loss: $81.4 million

· Fair Value Loss on Bitcoin Collateral Receivables: $171.4 million

The operating loss for the fourth quarter was $276.6 million, a significant increase from a loss of $0.7 million in the same period of 2024, primarily due to the downward trend in Bitcoin prices.

The net loss from ongoing operations was $285 million, compared to a net profit of $2.4 million in the same period last year.

The adjusted EBITDA was -$156.3 million, compared to $2.4 million in the same period last year.

The total revenue for the full year was $6.881 billion. Of this, the revenue from the Bitcoin mining business was $6.755 billion, with a total output of 6,594.6 Bitcoins for the year. Revenue from the international automobile trading business was $9.8 million.

The total annual operating costs and expenses amount to $1.1 billion.

Specifically, they include:

· Revenue Cost (excluding depreciation): $543.3 million

· Revenue Cost (depreciation): $116.6 million

· Operating Expenses: $28.9 million (including related-party expenses of $1.1 million)

· Miner Impairment Loss: $338.3 million

· Bitcoin Collateral Receivable Fair Value Change Loss: $96.5 million

The full-year operating loss is $437.1 million. The continuing operations net loss is $452.8 million, while in 2024, there was a net profit of $4.8 million.

The 2025 non-GAAP adjusted net profit is $24.5 million (compared to $5.7 million in 2024). This measure does not include share-based compensation expenses; refer to "Use of Non-GAAP Financial Measures" for details.

As of December 31, 2025, the company's key assets and liabilities are as follows:

· Cash and Cash Equivalents: $41.2 million

· Bitcoin Collateral Receivable (Non-current, related party): $663.0 million

· Miner Net Value: $248.7 million

· Long-Term Debt (related party): $557.6 million

In February 2026, the company sold 4,451 bitcoins and repaid a portion of related-party long-term debt to reduce financial leverage and optimize the asset-liability structure.

As per the stock repurchase plan disclosed on March 13, 2025, as of December 31, 2025, the company had repurchased a total of 890,155 shares of Class A common stock for approximately $1.2 million.

The US AI Startup Is Loving China's Open Source Model

Three Weeks of the US-Iran War: Who's Making Money, Who's Paying the Bill?

Interpreting Polymarket's Major Update Last Night: Fee Expansion, Self-Regulation, and New Incentives

From Human Application to Intelligent Collaboration: How GOAT Network Builds the Next Generation Digital Economy

CZ Washington Dialogue: Crypto Entrepreneurs are Accelerating Their Return to the United States

Morning Report | Strategy increased its holdings by 1,031 bitcoins last week; Katana Blockchain acquires IDEX; NYSE completes rule change to eliminate trading limits on crypto ETF options

Electric Capital: Tracking 501 types of yield-generating RWA assets, we discovered these patterns

Those who are cut off by AI will not disappear; they will become the creators of the next round of the economy

Stablecoins reshaping cross-border payments in Asia? Strategic panorama and investment opportunity analysis

Zuckerberg is building an AI agent to help him as CEO

Bloomberg: Swiss Private Bank Old Guard Rifts, Is Bitcoin the Spark?

Zuckerberg is building an AI assistant to help him be CEO

US AI Startup Goes All In on Chinese Mega-Model | Rewire News Morning Brief

Trump Lies Again: A "Five-Day Pause" Psyop, How Wall Street, Bitcoin, and Polymarket Insiders Synced Uposciogen

When a Token Becomes Labor, People Become the Interface

Ceasefire News Leaked Ahead of Time? Large Polymarket Bets on Outcome Before Trump's Tweet

BlackRock CEO's Annual Shareholder Letter: How is Wall Street Using AI to Keep Profiting from National Pension Funds?

Sun Valley Releases 2025 Financial Report: Bitcoin Mining Revenue Reaches $670 Million, Accelerating Transformation to AI Infrastructure Platform

On March 16, 2026, in Dallas, Texas, USA, CanGu Company (New York Stock Exchange code: CANG, hereinafter referred to as "CanGu" or the "Company") today announced its unaudited financial performance for the fourth quarter and full year ended December 31, 2025. As a bitcoin mining enterprise relying on a globally operated layout and dedicated to building an integrated energy and AI computing power platform, CanGu is actively advancing its business transformation and infrastructure development.

• Financial Performance:

Total revenue for the full year 2025 was $688.1 million, with $179.5 million in the fourth quarter.

Bitcoin mining business revenue for the full year was $675.5 million, with $172.4 million in the fourth quarter.

Full-year adjusted EBITDA was $24.5 million, while the fourth quarter was -$156.3 million.

• Mining Operations and Costs:

A total of 6,594.6 bitcoins were mined throughout the year, averaging 18.07 bitcoins per day; of which 1,718.3 bitcoins were mined in the fourth quarter, averaging 18.68 bitcoins per day.

The average mining cost for the full year (excluding miner depreciation) was $79,707 per bitcoin, and for the fourth quarter, it was $84,552;

The all-in sustaining costs were $97,272 and $106,251 per bitcoin, respectively.

As of the end of December 2025, the company has cumulatively produced 7,528.4 bitcoins since entering the bitcoin mining business.

• Strategic Progress:

The company has completed the termination of the American Depositary Receipt (ADR) program and transitioned to a direct listing on the NYSE to enhance information transparency and align with its strategic direction, with a long-term goal of expanding its investor base.

CEO Paul Yu stated: "2025 marked the company's first full year as a bitcoin mining enterprise, characterized by rapid execution and structural reshaping. We completed a comprehensive adjustment of our asset system and established a globally distributed mining network. Additionally, the company introduced a new management team, further strengthening our capabilities and competitive advantage in the digital asset and energy infrastructure space. The completion of the NYSE direct listing and USD pricing also signifies our transformation into a global AI infrastructure company."

"As we enter 2026, the company will continue to optimize its balance sheet structure and enhance operational efficiency and cost resilience through adjustments to the miner portfolio. At the same time, we are advancing our strategic transformation into an AI infrastructure provider. Leveraging EcoHash, we will utilize our capabilities in scalable computing power and energy networks to provide cost-effective AI inference solutions. The relevant site transformations and product development are progressing simultaneously, and the company is well-positioned to sustain its execution in the new phase."

The company's Chief Financial Officer, Michael Zhang, stated: "By 2025, the company is expected to achieve significant revenue growth through its scaled mining operations. Despite recording a net loss of $452.8 million from ongoing operations, mainly due to one-time transformation costs and market-driven fair value adjustments, the company, from a financial perspective, will reduce its leverage, optimize its Bitcoin reserve strategy and liquidity management, introduce new capital to strengthen its financial position, and seize investment opportunities in high-potential areas such as AI infrastructure while navigating market volatility."

The total revenue for the fourth quarter was $1.795 billion. Of this, the Bitcoin mining business contributed $1.724 billion in revenue, generating 1,718.3 Bitcoins during the quarter. Revenue from the international automobile trading business was $4.8 million.

The total operating costs and expenses for the fourth quarter amounted to $4.56 billion, primarily attributed to expenses related to the Bitcoin mining business, as well as impairment of mining machines and fair value losses on Bitcoin collateral receivables.

This includes:

· Cost of Revenue (excluding depreciation): $1.553 billion

· Cost of Revenue (depreciation): $38.1 million

· Operating Expenses: $9.9 million (including related-party expenses of $1.1 million)

· Mining Machine Impairment Loss: $81.4 million

· Fair Value Loss on Bitcoin Collateral Receivables: $171.4 million

The operating loss for the fourth quarter was $276.6 million, a significant increase from a loss of $0.7 million in the same period of 2024, primarily due to the downward trend in Bitcoin prices.

The net loss from ongoing operations was $285 million, compared to a net profit of $2.4 million in the same period last year.

The adjusted EBITDA was -$156.3 million, compared to $2.4 million in the same period last year.

The total revenue for the full year was $6.881 billion. Of this, the revenue from the Bitcoin mining business was $6.755 billion, with a total output of 6,594.6 Bitcoins for the year. Revenue from the international automobile trading business was $9.8 million.

The total annual operating costs and expenses amount to $1.1 billion.

Specifically, they include:

· Revenue Cost (excluding depreciation): $543.3 million

· Revenue Cost (depreciation): $116.6 million

· Operating Expenses: $28.9 million (including related-party expenses of $1.1 million)

· Miner Impairment Loss: $338.3 million

· Bitcoin Collateral Receivable Fair Value Change Loss: $96.5 million

The full-year operating loss is $437.1 million. The continuing operations net loss is $452.8 million, while in 2024, there was a net profit of $4.8 million.

The 2025 non-GAAP adjusted net profit is $24.5 million (compared to $5.7 million in 2024). This measure does not include share-based compensation expenses; refer to "Use of Non-GAAP Financial Measures" for details.

As of December 31, 2025, the company's key assets and liabilities are as follows:

· Cash and Cash Equivalents: $41.2 million

· Bitcoin Collateral Receivable (Non-current, related party): $663.0 million

· Miner Net Value: $248.7 million

· Long-Term Debt (related party): $557.6 million

In February 2026, the company sold 4,451 bitcoins and repaid a portion of related-party long-term debt to reduce financial leverage and optimize the asset-liability structure.

As per the stock repurchase plan disclosed on March 13, 2025, as of December 31, 2025, the company had repurchased a total of 890,155 shares of Class A common stock for approximately $1.2 million.